FinCEN Compliance Reporting - Full-Service Support from Start to Finish Learn More →

December 22, 2025

Mastering UCC Searches: A Comprehensive Guide for Title Professionals and Lenders

In the world of commercial real estate and lending, due diligence is everything. Whether you're a title agent preparing for a closing in New York, a lender evaluating collateral in Texas, or an attorney guiding a client through a multi-state deal, understanding how to conduct thorough UCC searches is essential. This comprehensive guide will walk you through the fundamentals of UCC searches, highlight complementary searches beyond the UCC, provide a step-by-step workflow, warn of common pitfalls (with real world examples), and explore the latest legal developments and technologies shaping UCC due diligence. By the end, you'll have practical checklists and insights to ensure your deals are iron-clad, even in high-volume states like California, Florida, New York, and Texas.

UCC Search Basics

What is a UCC search? A UCC search refers to examining public records for any Uniform Commercial Code (UCC) financing statements that name your debtor (borrower, buyer, or other party) as the debtor. UCC financing statements (often called UCC-1 filings) are legal notices filed by creditors to perfect security interests in a debtor’s personal property. In simpler terms, when a lender loans money secured by personal property (equipment, inventory, receivables, etc.), they file a UCC-1 to put the world on notice of their lien on those assets. UCC searches reveal these liens so that you know if the assets someone is offering as collateral or selling are already pledged to someone else.

Key features of UCC filings: UCC-1 financing statements are typically filed with a state’s Secretary of State (or similar filing office) in the state where the debtor is located or organized. They contain the exact legal name of the debtor, the secured party’s name, and a brief description of the collateral. Some important fundamentals include:

• Public Notice and Priority: A filed UCC-1 establishes the creditor’s priority in the collateral relative to other creditors. It’s a first come, first-in-line system – whoever files (or otherwise perfects) first generally has the first claim, which is crucial if the debtor defaults.

• Duration: UCC financing statements don’t last forever. They are effective for five years from the filing date unless a continuation statement (UCC-3) is filed to extend them an additional five years. Lenders must keep track of this timeline to avoid their lien lapsing.

• Scope of Collateral: UCC filings can cover all kinds of personal property. In commercial lending, it’s common to see “all assets” filings that encumber everything the debtor owns, as well as more specific filings (e.g., a lien just on a piece of machinery or on accounts receivable). Personal property under the UCC includes movable assets like equipment, inventory, vehicles, receivables, intellectual property rights, and even fixtures (items attached to real estate that can be considered personal property in some cases, like a commercial oven bolted in a restaurant).

• Where They’re Filed: Generally, UCC-1s are filed at the state level. For business entities, that usually means the state of incorporation/organization. For individuals, it’s typically the state of their principal residence. One exception is fixture filings, which are often filed in county land records where the property is located (more on that later).

Why are UCC Searches important?

They are a critical part of risk management in any secured transaction or property acquisition involving personal property. For example, a lender making a commercial loan will perform a UCC search on the borrower to ensure no other creditor already has a claim on the collateral being offered. Similarly, a buyer purchasing a company’s assets will want to search for UCC liens to avoid “buying” an asset that is serving as collateral for an unpaid debt. Title professionals handling commercial real estate closings also incorporate UCC searches, especially if the sale includes significant personal property or fixtures (say, a factory with installed machinery or a hotel with all its furniture and equipment). Skipping a UCC search could mean overlooking a lien that might surface later and derail a deal or lead to losses.

To put it in context, UCC filings are extremely common – hundreds of thousands are recorded each year, especially in economically bustling states like New York, California, Texas, and Florida. In these high-volume jurisdictions, it’s almost expected that any established business will have one or more UCC liens filed against it (for equipment loans, inventory financing, lines of credit, etc.). Conducting a UCC search is therefore standard practice in those states (and nationwide) whenever property or business assets change hands or new financing is being extended.

UCC Search results: When you perform a UCC search for a debtor’s name, you’ll retrieve any financing statement records associated with that name in the filing office’s index. A result typically includes the filing number, date, debtor name, secured party name, and often a summary of the collateral description. You may also see related UCC-3 filings (amendments, assignments, continuations, or terminations) attached to the original UCC-1 record. Part of the searcher’s job is to interpret these results: Which liens are active (still effective and not terminated or lapsed)? What collateral is described (is it a blanket “all assets” lien or something specific)? Who are the secured parties (could these be lenders that need to be paid off)? We’ll dive into the workflow soon, but keep in mind that a thorough UCC search review means identifying all open liens and understanding their implications for your transaction.

Before moving on, it’s worth noting that UCCsearches deal primarily with consensual liens (those that the debtoragreed to, like loans). However, not all liens come from loans and not all arecaptured by a UCC-1 filing. There are other types of liens and searches thatcomplement a UCC search – and failing to check those could leave a gap in yourdue diligence. Let’s explore those next.

Complementary Searches Beyond UCC

A UCC search is a powerful tool, but it doesn’t cover everything. To truly have ironclad due diligence, especially in commercial transactions, you should pair UCC searches with a few other key searches. Think of it as covering all your bases. Here are the main complementary searches you should consider beyond the UCC financing statement search:

• Tax Lien Searches: Tax liens are claims by government authorities for unpaid taxes. These can be federal tax liens (filed by the IRS for unpaid federal taxes) or state/local tax liens (for state income tax, sales tax, property tax, etc.). Tax liens are statutory liens, not consensual – the debtor doesn’t agree to them; they arise by law when taxes go unpaid. Often, tax liens are recorded in the same state filing office as UCCs (for example, many states let you search the Secretary of State’s records for tax liens against a debtor name, right alongside UCCs). However, in some cases they might be filed locally (county level) or in separate registries.

Why search for them? Because tax liens typically have priority over other liens and can attach to all of a debtor’s property. If you’re lending against or buying assets, a surprise IRS lien can wreak havoc with priorities. Always check if the debtor has any outstanding tax liens — it will signal a serious claim that likely needs to be paid off or addressed.

• Judgment and Litigation Searches: A judgment lien results from a court judgment against the debtor (for example, if someone sued the debtor and won a money judgment, they may file a judgment lien to attach the debtor’s property). Like tax liens, judgment liens are not recorded as UCCs but often are filed in state or county records. A related task is to search for pending lawsuits or litigation involving the debtor. Even if a case hasn’t yet resulted in a judgment, knowing if your debtor is being sued (or has hefty judgments) is valuable context.

Many due diligence processes include a civil litigation search (checking court records for any cases involving the debtor’s name) and a specific judgment lien search (which might be at county level where the debtor resides or does business). These searches help uncover any legal troubles that could lead to liens or indicate financial distress.

• Bankruptcy Search: If a debtor has filed for bankruptcy, it dramatically affects what you can or cannot do with their assets (due to the automatic stay and bankruptcy estate rules). A bankruptcy search (usually done by checking federal bankruptcy court records or using a service) will show if the debtor is in an active bankruptcy or has recent bankruptcy cases. This is crucial because a bankruptcy filing could invalidate certain unperfected liens or change priorities, and it means any transaction needs court approval. Even if you find no UCC liens, a bankruptcy could impose restrictions or reveal that liens were discharged or avoided in the case.

• Entity and Standing Checks: It’s also wise to verify the debtor’s legal name and status. This might involve searching the state’s corporate registry to confirm the exact name (for accuracy in your UCC search) and ensure the company is active and in good standing. While not a “lien” search per se, getting the name right is so fundamental that it’s worth double-checking via the incorporation records. (Many UCC search failures trace back to searching the wrong name or a typo – we’ll see more in pitfalls.)

• Fixture Filings and Real Property Records: As mentioned, fixtures (personal property that is attached to real estate, like a furnace, manufacturing equipment bolted to the floor, or solar panels on a building) can be a bit of a hybrid. Under the UCC, a creditor can file a fixture filing in the local real estate recording office (county recorder or clerk) to ensure their lien on the fixture is discoverable by anyone doing a real estate title search. These filings are still governed by the UCC, but they may not show up in a state level UCC search.

So if your transaction involves significant fixtures or if you’re dealing with a specific piece of equipment at a property, you should search the county records in the property’s location for any UCC fixture filings or other liens. For example, a large industrial AC unit or a piece of restaurant equipment might have a UCC filed in county land records – missing it could mean a new property owner ends up subject to a prior lien on those fixtures.

• Other Specialized Searches: Depending on the nature of the deal, there may be other searches to consider. For instance, if intellectual property (patents, trademarks) is a key asset, you might search the U.S. Patent and Trademark Office databases for any recorded security interests or assignments. If vehicles are collateral, a search of the state motor vehicle department for liens might be prudent (though often those liens appear on titles rather than UCCs). These are more situational, but the guiding principle is to think broadly about what claims could exist outside the UCC system and check those sources.

In summary, a UCC search should be one part of a broader due diligence toolkit. In fact, many professional due diligence firms or title support companies (like Skyline Title Support) offer combined lien search packages that bundle UCC, tax lien, judgment, and bankruptcy searches into one report. The goal is to leave no stone unturned. For example, rarely would you search UCC records without also checking for tax liens – the two go hand-in-hand in painting the full picture of encumbrances on a debtor’s assets. By covering these complementary searches, you significantly reduce the risk of an unpleasant surprise emerging later.

Now that we’ve outlined what to search, let’s turn to how to actually conduct a UCC search from start to finish, incorporating many of these elements into a straightforward workflow.

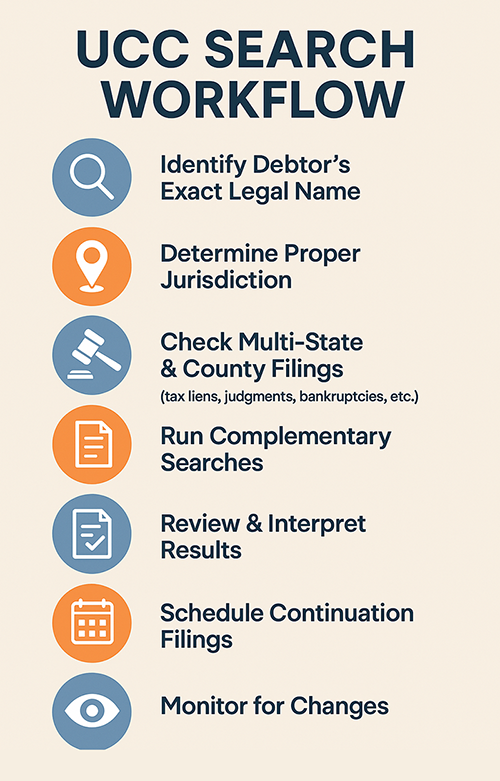

A Step-by-Step UCC Search Workflow

Performing a UCC search (along with related searches) can be broken down into clear steps. Following a structured workflow ensures consistency and minimizes the chance of missing something critical. Here’s a step-by-step guide:

1. Identify the Debtor’s Exact Legal Name: UCC searches are conducted by debtor name, so getting the name exactly right is crucial. For a company, use the official name registered in its formation documents (including punctuation, spacing, suffix like Inc, LLC, etc.). For an individual, use the name exactly as it appears on their state issued ID (many states’ laws specify this for individual debtor names). Tip: Check the debtor’s name via a corporate registry or request official ID copies to avoid any spelling mistakes or name variation.

If the debtor has former names or trade names, note those too – while UCC filings should be under the exact current legal name, it may be worth searching old names if a business recently changed its name (or an individual changed their name) to catch any filings still indexed under those. A small typo or variation in the name can cause a UCC search to come up empty even if liens exist, so double check spelling and formatting. (As an example, “ABC Solutions, Inc.” is not the same as “ABC Solution Inc” in the UCC index – that missing “s” or a misplaced comma could make or break your search results.)

2. Determine the Proper Jurisdictions to Search: Next, figure out where you need to search. Under UCC rules, typically you search the state where the debtor is located. For organizations, “located” usually means the state of incorporation/organization. So if your borrower is a Delaware LLC operating in California, the main UCC search would be in Delaware (since that’s where a UCC-1 should be filed for that company). However, due diligence might not stop at one state. Consider other jurisdictions: If the company has a chief executive office or principal place of business in another state, some practitioners also search that state for any tax liens or local filings.

If the transaction involves fixtures or real estate related collateral, include a search of county records where the property is located. If the debtor recently moved from or was organized in another state within the last few years, you might search the old state as well (UCC filings remain effective even after a move, for a grace period, and some liens could still be of record in the old state). For individuals, search their state of residence (and perhaps any recent former residence state if they moved).

Essentially, think about any state where a lien could feasibly be filed against the debtor or its property, and ensure those are covered. It’s better to cast a slightly wider net than to miss a filing in a less obvious place. For example, for a business debtor in Florida that is a Delaware corporation, you’d search Delaware for UCC filings, and also search Florida’s records for any tax liens or judgments under the company name (since Florida might have a state tax lien even though UCCs are in DE). Multi-state searching is common, and using a service that can do a national search by name can be very helpful here.

3. Conduct the UCC Search at the Filing Office: With the names and jurisdictions in hand, it’s time to run the UCC search in the official databases. Most states have an online UCC search system through the Secretary of State or equivalent office. You’ll enter the debtor’s name and retrieve matches of any financing statements. When doing this: Use the standard search logic if available (some states have a dedicated search function that follows Article 9 rules for what constitutes a match, ignoring punctuation and trivial differences). If you’re using an online system, carefully follow their instructions for formatting the name. - Consider ordering an official (certified) search from the state if you need guaranteed results. State filing offices can provide certified search results for a fee, which will list all UCC filings found under the name using the state’s official search algorithm.

This can be important if you need the results for a legal closing or just for extra certainty. Retrieve copies of the filings, if possible. Seeing the actual UCC-1 forms and any attachments (collateral descriptions) will allow you to fully understand each lien. Many state online systems let you download PDF copies of filings for a small fee. If not, you can request them or use a third-party service. - Repeat for each jurisdiction identified. For instance, search the Delaware UCC records for “ABC Solutions, Inc.” and then search the Florida Secured Transaction Registry for the same name (which might show state tax liens, etc., in Florida’s index). Also search any relevant county for fixture filings (which often means using the county’s grantor-grantee index or a title search system under the debtor’s name).

4. Search for Tax Liens and Other Liens in Parallel: While you’re searching UCC records, you should also search for tax liens, judgments, and bankruptcy records as separate steps (if those aren’t automatically included). Some states’ UCC search systems will also show state level tax lien filings by name – make sure to include those results. However, federal tax liens might be filed in a separate index or at the county level. It’s a good practice to: Check the debtor name in any available tax lien database. For federal tax liens, many states file them with the Secretary of State (e.g., Texas and California do, making them visible in a state search), but others file in counties. If unsure, a search of county records in the debtor’s principal location for “Internal Revenue Service” or the debtor’s name can reveal IRS liens. Alternatively, there are nationwide lien search services that will check multiple sources.

Perform a judgment lien search. This may involve searching the debtor’s name in county court records or judgment indices where the debtor resides or does business. If your debtor is a company, search in its home county; if an individual, in the counties where they live or have property. Run a bankruptcy search for the debtor’s name in the federal bankruptcy court system (PACER or a consolidated bankruptcy search tool). Even a quick web search of “Debtor Name + bankruptcy” can sometimes flag news, but a formal search is best. Consider a general litigation search if the deal is substantial – this could involve checking state court databases for any pending lawsuits naming the debtor (which could be under civil, criminal, or probate, depending on context).

Essentially, step 4 is about covering the “beyond UCC” stuff we discussed in the previous section as part of your workflow. You might handle this simultaneously or immediately after the UCC search. Modern search platforms often allow you to order a bundle that checks all these categories at once.

5. Review and Analyze the Results: This is a critical step – raw search results only help if you interpret them correctly. Go through each finding carefully: List out active UCC filings: Which UCC-1 financing statements are currently effective? Remember, if the filing date is more than five years old, check if there’s a continuation; if not continued, it may have lapsed (though often it will still appear in search results for some time after lapse). Look at each active UCC’s collateral description. Is it a blanket lien on “all assets,” or something specific like “equipment listed on Schedule A”? Identify what assets are encumbered and who the secured party is. If your transaction requires free and clear assets, any “all assets” UCC is a red flag to address. Note any terminations or amendments: If a UCC filing shows a termination (UCC-3 Termination) filed, that means the secured party released their claim on record. Terminated UCCs are usually considered inactive (even if technically they might show up until they drop off the index).

Use these to distinguish which liens are actually still claims. Amendments and assignments should also be read: for example, an amendment might change the debtor’s name (alerting you to search under a new name too), or an assignment might indicate the loan was sold to another lender (so the secured party of record changed). Examine dates and continuity: Pay attention to filing dates relative to your deal. If you see a very recent UCC filing (say, last month) and your debtor didn’t mention taking a new loan, that’s something to investigate. Conversely, if a UCC is about to lapse (maybe will expire next month), that might influence whether it will remain by closing (though you can’t assume it will lapse and go away – many will be continued).

Check the complementary search findings: Did the tax lien search show anything? For instance, if you discover a federal tax lien against the debtor for $100,000 filed last year, that’s crucial information. It likely attaches to all the debtor’s property. If you’re representing a lender, that tax lien would typically have priority over a new UCC filing (tax liens often trump later security interests) unless it’s addressed. Similarly, review any judgment liens or litigation. A judgment lien for a large sum may mean the debtor has financial troubles or that any sale will require dealing with that lien payoff.

Bankruptcy hits: If the debtor is in bankruptcy, all bets are off until you figure out the status (and you’d typically handle that very differently – possibly even halting any transaction or ensuring bankruptcy court approval). If there’s a recent bankruptcy that’s closed, see if liens were discharged or if the debtor emerged with certain liens intact.

At this stage, it’s wise to create a summary or checklist of findings. For example: "3 active UCC financing statements found in Delaware: (1) Filing #123456 covering all assets by Big Bank, filed Jan 2022; (2) Filing #234567 covering specific equipment by Equipment Lender, filed Mar 2023; (3) Filing #345678 covering accounts receivable by Factor Corp, filed Aug 2024, but terminated Jun 2025." "Federal tax lien of $15,000 filed by IRS in July 2021 in Florida (Duval County) against debtor for unpaid 2019 taxes." "No judgment liens found in Delaware or Florida under debtor’s name. No bankruptcy filings found. One pending lawsuit noted in Florida State Court (a contract dispute case, no judgment yet)."

This kind of clear breakdown helps everyone involved understand what’s out there.

6. Address and Resolve Issues (Next Steps): The final “step” in the search process goes beyond just finding information – it’s about acting on it. Once you know what liens and risks exist, plan how to handle them in your transaction: For a lender extending new credit: You might require that any prior UCC liens discovered be terminated or subordinated. If there’s an existing secured loan that will be paid off with your loan, work with that prior lender to get a payoff letter and a commitment to file a UCC-3 termination upon payoff. If certain collateral has an outstanding lien (like equipment financed by another lender), decide if that’s acceptable or if that needs clearing. Also, if a tax lien exists, perhaps part of your loan proceeds must go to clearing that tax debt (since the IRS lien could otherwise prime your interest).

For a buyer in an acquisition: If you find UCC liens on assets you’re buying, you’ll likely make the sale contingent on those liens being released. That could involve using sale proceeds to pay the secured debt and obtain terminations. Your closing checklist should include getting all necessary UCC termination statements filed or in escrow. In some cases, you might negotiate indemnities or escrows for liens that can’t be cleared immediately. Coordinate with title insurance or legal counsel: In a real estate closing that includes personal property, the title company might not insure over certain UCC or lien issues, so they need to be resolved.

Title agents often collect the UCC search results early so that any problematic liens can be dealt with before closing day.

Future proofing: If you’re the secured party (lender), ensure you file your own UCC-1 correctly (using that exact debtor name we emphasized) once you close the deal, to perfect your interest going forward. And diarize the continuation deadline (five years minus a few months) to avoid your lien becoming a pitfall (as we’ll see, failing to continue a UCC can lose your priority).

By following these steps, you create a robust UCC search workflow. It moves from preparation (getting names and jurisdictions right), through execution (searching the records thoroughly), to analysis (making sense of results), and finally to action (clearing or mitigating any issues found). Especially on complex deals with multiple parties or multi-state assets, a checklist driven approach is invaluable. In practice, many professionals will use a UCC search checklist to track tasks:

✅ Debtor name confirmed (correctspelling, exact legal name).

✅ Searched state of incorporation (e.g., Delaware SOS) – results obtained.

✅ Searched state of principalbusiness (e.g., Florida) – results obtained, including tax liens.

✅ Searched relevant county records (Duval County fixture filings/tax liens) – results obtained.

✅ Searched federal tax lien indexor records – no liens (or liens found, noted).

✅ Searched for judgments in XCounty – none (or noted).

✅ Bankruptcy PACER checked – norecord (or noted).

✅ Copies of all UCC filings pulledand reviewed.

✅ All active liens summarized andcommunicated.

✅ Plan made for payoff/terminationof Filing #123456 and IRS lien at closing.

Such a checklist keeps everyone on the same page and ensures nothing slips through the cracks.

Even with a great process, however, there are still pitfalls to be aware of. In the next section, we’ll discuss some common mistakes and cautionary tales that underscore why meticulous attention to detail in UCC searches is so important.

Common Pitfalls from Real World Cases

Despite best efforts, mistakes in UCC searches or filings do happen – and they can lead to serious consequences. Let’s look at a few common pitfalls, illustrated by real world scenarios, so you know what to watch out for:

• Name Errors Can Be Deal Breakers: The #1 pitfall in UCC practice is a debtor name mistake. For example, a lender intended to file a UCC against “Thomas A. Smith Enterprises, LLC” but mistakenly listed the debtor as “Tom A. Smith Enterprises LLC” on the financing statement. That small difference meant that in a standard search for the correct legal name, the filing didn’t show up. In a real case in Delaware, a missing period in a debtor’s name on a UCC-1 (omitting “Inc” after the name) caused the secured party’s interest to be deemed unperfected – the court held the financing statement “seriously misleading” because a search under the debtor’s actual name didn’t reveal it.

The lender effectively lost its collateral to another creditor due to a minor typo. Lesson: Always get the name exactly right on filings, and when searching, consider ordering official searches which use the filing office’s algorithm (which might catch some variations, but not all). Even something as trivial as an extra space or a missing letter can hide a UCC filing from search results. If you’re searching and have any doubt about name variations (say the debtor sometimes goes by a shortened name), run additional searches just in case. It’s better to have a few “false hits” from broad searching than to miss the one real lien because of a name nuance.

• Not Searching All Locations: Imagine a business headquartered in California but incorporated in Delaware. A lender only searched California’s UCC records and found no liens, so they extended a loan. It turned out the borrower had a prior loan and UCC filed in Delaware (under the correct rule of state of incorporation). The lender didn’t discover it until the borrower defaulted and the Delaware filed creditor showed up claiming the assets. This scenario underscores the pitfall of choosing the wrong jurisdiction or not searching all the necessary ones. We’ve seen cases where creditors assumed filing in the state of the head office was enough, but Article 9’s rules pointed to a different state.

Conversely, for searchers, if you only check one state when the debtor has multi-state connections, you can miss liens. Lesson: Follow the location rules strictly (state of organization for entities, etc.), and when in doubt, search any state that has a logical connection to the debtor (prior locations, major asset locations, etc.). Don’t forget county level searches for fixtures if applicable. In one Florida transaction, a fixture filing at the county for restaurant equipment was missed because the searcher only checked the state UCC registry – the lien surfaced later, complicating the sale. Thorough due diligence means covering all bases geographically.

• Overlooking Tax Liens and Statutory Liens: A common mistake is to focus solely on UCC filings and ignore other liens that might be sitting out there. Consider a case where a lender did a UCC search on a borrower in New York and found no financing statements. The loan closed, secured by the borrower’s inventory. Unfortunately, the borrower had a sizable IRS tax lien that the lender hadn’t checked for. When the borrower later faced IRS enforcement, the IRS lien had priority on that inventory, and the lender’s claim was at risk. Tax liens typically superprioritize even if filed later in time, so missing them is dangerous. Similarly, judgment liens can sneak up.

Lesson: Always include tax lien and judgment searches as part of the process (which is why we highlighted it earlier). Many “real world” horror stories of hidden liens involve something like a surprise tax lien, not a UCC, precisely because someone assumed “no UCC filings = no liens” which isn’t true. Even seasoned attorneys can slip up if they’re not used to checking every category.

• Misinterpreting Search Results: Sometimes the data is there, but we fail to interpret it correctly. For instance, a UCC search might show an amendment or continuation that’s easy to gloss over. In one case, a search report showed a UCC-1 filed by a bank five years ago and a UCC-3 filed by the same bank recently. The searcher assumed the UCC-3 was a termination and concluded the lien was gone – but actually it was a continuation, meaning the lien was very much still active. This error wasn’t caught until closing when the title company raised an issue. Lesson: Pay attention to the details of each record – is it a termination or continuation?

If unfamiliar with the forms, note that a continuation extends a lien (good for the secured party, bad for a new one), whereas a termination explicitly says the debtor is released. Another misinterpretation pitfall is collateral descriptions: seeing a specific collateral list and assuming it doesn’t affect your deal when in fact the described assets might overlap with what you’re dealing with. For example, a filing might only mention “equipment financing for printing press #123” – if you’re buying that very printing press, that lien matters a lot. Context is key.

• Timing and Update Issues: UCC searches are a snapshot in time. A pitfall is conducting your search too early and not updating it. Imagine you pulled a UCC search 90 days before closing on a loan. Between that search and the closing, the debtor could have incurred a new loan and a new UCC filed that you wouldn’t know about unless you research. Real case: a lender pulled a search in the spring, and by summer when the deal funded, the borrower had quietly gotten an equipment loan.

The new UCC was filed a month before closing, but since the lender didn’t run an update, they closed without knowing and ended up second in line on that equipment. Lesson: Do your initial searches early to identify issues, but if there is a gap of more than a few weeks (or any significant gap) before closing, run bring-down searches or updates closer to the closing date. Many practitioners will pull a fresh search the day before or day of closing to catch any last minute filings. It’s cheap insurance.

• Failure to Continue or Release Own Filings (for Secured Parties): This is more of a pitfall for lenders themselves but is worth noting. If you are a secured party, failing to continue your UCC-1 before it lapses at five years means your lien becomes unperfected. There have been cases where lenders calendared the wrong date or simply overlooked the deadline – and a day after lapse, a debtor’s new creditor filed their own UCC, leaping into first position. The original lender was left scrambling, often ending up unsecured in bankruptcy because their financing statement had lapsed.

On the flip side, if a loan is paid off but the UCC termination isn’t filed, that can cause headaches for the debtor later (they’ll see an “open” lien on record that’s actually satisfied, but it takes effort to clear it). Lesson: For lenders – maintain good tickler systems for continuations; for searchers – check those dates carefully and if you see a lapsed UCC, you might need to confirm if it was truly allowed to lapse or if an administrative error happened (sometimes filings don’t show up but were done, etc.). And if you’re representing a borrower or buyer and a paid-off lien hasn’t been terminated, push to get that termination filed to avoid lingering clouds on records.

These pitfalls show why a detail oriented approach and some healthy skepticism are valuable in UCC due diligence. If something seems off (e.g., “why would a company with lots of assets have zero UCC filings? Is it really debt-free or could its name be listed slightly differently?”), trust your instincts and double-check. Use real-world cautionary tales as motivation to triple-check names and search multiple ways.

One more example combining a few pitfalls: A commercial broker in Florida was helping sell a portfolio of restaurant assets. The initial lien search came back “clear” except for one small equipment lease. They proceeded to closing, only to have a last minute discovery: the seller had an alias LLC name under which a blanket UCC was filed (the seller failed to mention this separate LLC they used). The lien was missed because the search was only under the primary business name. The sale was delayed for weeks as they negotiated with that creditor to terminate the lien. This highlighted issues of name variations and incomplete info from the client – always ask if the debtor has used any other names or entities and consider searching those if so.

By learning from common mistakes, you can avoid them. Now, beyond practical pitfalls, it’s important to stay aware of changes in the legal landscape that could affect UCC searches. In recent years, Article 12 of the UCC has been a hot topic due to what it means for new types of assets. Let’s discuss that next.

Article 12 Legal Developments and Their Impact

The Uniform Commercial Code isn’t static; it gets updated to address new types of commerce. The latest major update is the introduction of UCC Article 12, a completely new article aimed at handling emerging digital assets. If you haven’t heard of it yet, you likely will soon, as many states are adopting these changes. Here’s what you need to know:

What is Article 12 about?

Article 12 (sometimes referred to as the 2022 UCC Amendments) provides a legal framework for controllable electronic records, which is legal-speak for certain digital assets like cryptocurrencies, NFTs (non-fungible tokens), and other electronic tokens that can be owned and transferred. These are assets that aren’t physical, yet people offer them as collateral or sell them, and prior to Article 12 the UCC didn’t clearly address how to perfect security interests in them or how buyers could be protected when acquiring them. Article 12 defines concepts like a “Controllable Electronic Record” (CER) and gives criteria for having control of these digital assets, somewhat analogous to possessing a physical good or a negotiable instrument.

One key feature introduced is a “take free rule” for digital assets: under Article 12, a good faith purchaser of a controllable electronic record can take it free of prior claims if they obtain control of it without notice of those claims. This is similar to how a person who buys a physical good in good faith can often take it free of unknown security interests (or how a bona fide purchaser of a negotiable instrument takes free of certain claims).

Before Article 12, if an asset like bitcoin was used as collateral and then transferred, the security interest would follow it everywhere and it was nearly impossible for a later buyer to know about or avoid that lien (since blockchain transactions are pseudonymous and UCC filings by debtor name are impractical to link to a specific bitcoin). Article 12’s rules aim to fix that dilemma.

Why does Article 12 matter for due diligence?

As Article 12 gets enacted in various states, it means that new types of collateral might not rely solely on UCC-1 filings in the traditional sense. Here are some impacts to consider: New collateral categories: The amendments include new terms like controllable accounts and controllable payment intangibles, which essentially are rights to payment evidenced by these electronic records. If your transaction involves any kind of cryptocurrency, digital tokens, or even certain electronic payment obligations, the way to perfect a lien on those might be via obtaining “control” (a bit like how you perfect a lien on investment securities by control, not just filing). So a UCC search might not reveal a prior interest in a digital asset; instead, you’d need to investigate if someone else has control of it (for example, if a third party custodian holds the keys for another lender).

Article 12 is state law – adoption varies: By mid 2025, a large number of states have enacted the Article 12 amendments (roughly half the states, including big ones like California and Illinois, as well as Delaware which is significant since so many businesses are incorporated there). Other states, like New York, have legislation pending or are expected to adopt soon. For a period of time, there will be a patchwork where some states’ UCC laws include Article 12 and others don’t.

This can create choice-of-law complexities. For instance, if a digital asset is involved and you’re dealing with a state that hasn’t adopted Article 12 yet, the rules of older Article 9 might apply differently, especially for where to file or how to perfect. But broadly, the trend is that most states will adopt these provisions by 2025–2026, modernizing the UCC everywhere.

Due diligence for digital assets: If you’re a lender considering digital assets as collateral (which might still be relatively niche for title agents, but increasingly relevant in commercial lending), you need to update your procedures. Instead of (or in addition to) filing a UCC-1, you might require the borrower to transfer the crypto into a controlled wallet where you hold the key – that gives you control (per Article 12) and priority. For someone investigating liens, it means you can’t just search the Secretary of State and call it a day. You may need to ask questions like, “Are any of your assets cryptocurrency or tokenized assets? If so, has anyone else been given control or are they held with any third party platform?” There won’t be a public record in the UCC system disclosing that kind of arrangement because Article 12 doesn’t require public filing if control is how you perfect.

This is similar to how a bank’s security interest in a deposit account is perfected by control (account control agreement) – you won’t find a UCC filing for it. So due diligence might involve reviewing control agreements or contracts, not just searching databases. Good news for buyers: From a purchaser’s perspective (say, buying digital assets or a business that includes them), Article 12’s take free provisions mean if you acquire a CER for value without knowing of a claim, you might take it free and clear. This reduces the burden on purchasers to do exhaustive lien searches for digital assets (which previously was not even feasible – you can’t search a blockchain for a lien). Over time, this could simplify certain transactions. But in transitional times, caution is still warranted: until everyone’s on Article 12 and the case law is established, parties may still contractually require representations about digital assets being lien free, etc.

Legal complexity and state differences

One thing to be aware of is the potential for choice-of-law issues during the transition. Article 12 includes a provision that the governing law for digital asset collateral can be chosen by the parties (to some extent) – a debtor and secured party can pick a jurisdiction’s law to govern perfection by control of a digital asset, even if that jurisdiction has no other connection, presumably to choose a state that adopted Article 12. This is novel because normally under Article 9, the law of the debtor’s location governs. If not widely adopted, there could be conflicts: e.g., a lender might pick Delaware (with Article 12) as the governing law for a crypto collateral agreement to be sure they’re covered, but if the debtor is in a state without Article 12, will a court there honor that choice? These nuances are more of a concern for the lawyers structuring deals than for performing a search, but it’s good to know the landscape is shifting. For our purposes, staying updated is key. When you perform lien searches or prepare documentation, you’ll want to know if the state you’re dealing with has enacted the new UCC amendments or not, as that might affect what you’re looking for or what steps the secured parties take.

In practice so far

As of 2025, Article 12 is still brand new in most places. We are starting to see transactions where lenders explicitly mention it – for example, a loan agreement might say “the borrower shall take all steps to ensure the secured party obtains control (as defined in UCC Article 12) of any cryptocurrency collateral.” From a title support perspective, if such collateral is present, there may be less to “search” and more to verify contractual control. But you might still find filings that use new terminology. The updated UCC forms (in states that adopted) might allow indication of a CER or controllable account as collateral. So you might begin seeing UCC-1 descriptions like “all controllable electronic records, including cryptocurrency wallet [address]” etc. Knowing what “CER” means when reading a filing is helpful – that’s Article 12 jargon for digital assets under control.

To sum up, Article 12 is bringing the UCC into alignment with modern technology. The impact on due diligence is that simply searching debtor names in public records may not suffice for certain assets anymore. It places more importance on asking the right questions of the parties and understanding how digital assets are held. It’s an evolving area, so it’s wise for lenders and attorneys to get educated on their state’s adoption status and any new procedures. Title agents and brokers should at least be aware that if someone mentions crypto in a deal, a call to counsel is in order to ensure proper steps are taken (since it won’t be just a normal UCC-1 filing scenario).

As the legal framework evolves, so do the tools and technology we use to perform searches and manage liens. In the final section, we’ll look at some of the new technologies and innovations that are changing how UCC due diligence gets done, making the process more efficient and accurate.

New Technologies in UCC Due Diligence

UCC searches and filings have come a long way from the days of paper files and courthouse visits. Today, technology is playing a major role in streamlining lien searches, improving accuracy, and saving time. Title professionals, lenders, and attorneys are increasingly leveraging these tools to enhance their due diligence process. Here are some of the exciting technologies and trends in the UCC search world:

• Automation and AI Powered Search Analysis: One of the most significant advancements is the use of artificial intelligence (AI) and machine learning to analyze UCC search results. When you run a UCC search for a busy company, you might get back dozens of filings, each with multiple pages of details. Traditionally, an expert would manually read through all those to piece together which liens are active, which assets are encumbered, and if there are conflicts.

Now, AI driven tools can do a lot of the heavy lifting. For example, there are software solutions (used by leading lien service providers) that will take all the raw UCC filings and generate an organized report highlighting key information: how many active liens were found, which collateral is mentioned most frequently, what the chain of filings on each loan is (original, amendments, continuations, terminations), and even flag potential issues like duplicate filings or inconsistencies.

This kind of actionable intelligence means instead of wading through 100 pages of UCC documents, a lender or attorney might get a dashboard or summary that says, “Debtor X has 5 active liens: 2 are purchase money on specific equipment, 3 are blanket liens by banks; Lien #1 and #3 both claim inventory – potential conflict.” The AI can consolidate multiple borrower searches too (say a loan has co-borrowers, you search each, the system can merge the results to show a combined picture). This speeds up decision making tremendously. Lenders in particular love this because it helps them quickly assess lien priority and determine if the collateral is already heavily encumbered. It also reduces human error; the AI is less likely to overlook an amendment or miss that “Corp” vs “Corporation” in a name is the same entity.

• Standardized Digital Reports and Data Extraction: New tech tools provide standardized reports where all the key fields from UCC filings are extracted and laid out neatly. For example, rather than relying on a person to note the dates, an automated system will list each filing’s date, file number, debtor name, secured party, collateral summary, lapse date, etc., in a spreadsheet or report format. This makes it easy to scan and spot what you need. These reports often include interactive features – e.g., click a lien to see its full history and related documents.

By having everything in one place, organized, a due diligence team can ensure nothing is missed. If you've ever tried to manually trace a lien that has, say, one continuation and two amendments (perhaps changing the secured party), you know it can be confusing. Now systems can chain these for you automatically, showing the “family tree” of a financing statement from origination to the latest update. This reduces the chance of misinterpreting records because the software keeps track of which amendment belongs to which initial filing, etc.

• Integration with Closing and Loan Platforms: Title agencies and lenders often use comprehensive software platforms to manage closings or loan originations (for instance, title production software or loan origination systems). Modern UCC search services (like Skyline Title Support and others) frequently provide integration via API or direct plugins into these platforms. That means, from within your closing software, you might be able to click “Order UCC Search” and have the request automatically sent out, then receive the results back into your system. This saves double entry of data and speeds up workflows.

If you’re a title agent working on a transaction in, say, Qualia or Resware (popular title software), having an integration with your lien search provider allows you to seamlessly request a multi-state UCC search and get the report attached to your file without ever logging into a separate website. These integrations also help with consistency – fewer typos in orders, since data can autofill from your file (again, ensuring the debtor name is exactly as you entered in your system). For lenders, integration means their loan officers or analysts don’t have to go to multiple websites to gather due diligence; it can be built into their underwriting workflow.

• Real Time Search Capabilities and Databases: The speed of search has improved drastically. Many states now have real time online UCC databases accessible 24/7. What used to require faxing a request to a state office and waiting days can often be done in minutes online. Additionally, some technology companies aggregate UCC data from all states to create essentially a one stop national UCC search database. While not every state allows complete third-party aggregation, a lot of data is available that way.

This means a comprehensive multistate search that might have taken a week by manual requests can potentially be done almost instantly. Real time access is critical when you’re on a deadline, and it’s becoming the norm. Moreover, search algorithms have improved – they can handle fuzzy logic to catch name similarities in some systems (although officially, exact legal name is used, some search tools will suggest “Did you mean X Corp Inc?” if no results under X Corporation, for example).

• Monitoring and Alerts: Another tech development is continuous lien monitoring services. Let’s say you’re a lender who has made a loan and filed your UCC. Wouldn’t it be nice to know if another creditor files a new UCC against your borrower a month or year later? There are services now that will monitor a given debtor name and send you an alert if any new filing appears in the public record. This is helpful for risk management – it can be an early warning that your borrower might be taking on additional secured debt (which could violate loan covenants or just increase your risk).

Similarly, monitoring can alert you when a rival creditor continues their UCC (meaning they plan to stick around) or if someone files a termination (maybe the debt got paid off – which could be an opportunity if you want to lend more, etc.). For buyers or investors, monitoring can be set during a deal interim period, to make sure no new liens pop up between the initial search and closing (as we mentioned in pitfalls, timing matters – tech can assist by autochecking daily). This kind of ongoing due diligence was cumbersome before but now is easy to automate.

• Blockchain and Future Registry Innovations: Looking further ahead, some experts envision blockchain technology playing a role in UCC filings and transfers. A blockchain could serve as a decentralized registry for certain types of assets or liens, providing real time, immutable records. For example, there are pilot programs and discussions about using blockchain for managing fixtures or specialized collateral so that searching becomes more unified. While this isn’t mainstream yet, a few states have explored using blockchain for government recordkeeping.

The interplay of Article 12 and blockchain is particularly interesting: one could imagine a future where a digital asset collateral registry is a blockchain that lenders and debtors use to register claims, which might then automatically clear when assets move to a buyer who qualifies for take free under Article 12’s rules. We’re not there yet, but it’s a space to watch. At present, the more concrete tech is what we discussed above (AI, automation, integration).

• User Friendly Tools for Small Firms: Not all new tech is only for big banks. There are also simpler web based tools that even solo attorneys or small title companies can use to run UCC and lien searches with ease. These interfaces guide the user through the process, helping validate debtor name spellings (some will check the Secretary of State corporate database for you to ensure you typed the name correctly), automatically searching multiple jurisdictions in one go, and organizing results. The cost of these tools has come down, making them accessible beyond just large financial institutions.

This democratization of advanced search tech means better due diligence across the board, as even a one person firm can leverage sophisticated search algorithms and databases that weren’t available years ago without a hefty contract.

• Reducing Turnaround Time and Human Error: Ultimately, the benefit of all this technology is that UCC due diligence can be done faster and with fewer mistakes. Automation reduces the chance of a typo causing a missed lien. AI analysis reduces the risk of an overworked analyst accidentally skipping page 45 of a long report where a critical detail is buried. And quick turnarounds mean even last minute checks are feasible, enhancing protection. This helps deals close on time and with confidence. For example, with an AI generated lien analysis, a lender might cut down a process that took two days of poring over documents into an hour of review, allowing them to respond to clients quicker and allocate expert time to really thorny issues rather than routine info gathering.

In practical terms, if you’re a titleagent or attorney, it’s worth exploring what solutions your search providersoffer. Many, like Skyline Title Support, incorporate these technologiesinto their services. You might receive not just raw copies of UCC filings, but a polished summary, or have the ability to log into a platform and see yoursearch results in a dashboard format. Embracing these tools can give you anedge in thoroughness and efficiency.

Staying informed on both the legal developments (like Article 12) and technological advancements ensures that your UCC due diligence remains robust, up-to-date, and efficient. The landscape of secured transactions is evolving with the digital age, but the fundamental goal remains the same: to uncover any interests or claims on assets before a transaction happens, so they can be handled and your deal can proceed smoothly.

How Skyline Title Support Can Help

At Skyline Title Support, we understand how vital comprehensive UCC due diligence is for protecting your deals. Our team of experienced professionals conducts UCC searches nationwide, including the high volume states of New York, California, Texas, Florida and beyond. We don’t just stop at the UCC financing statements – our services include searching for tax liens, judgment liens, bankruptcy records, and even county-level filings for fixtures, so you get the complete picture every time.

Leveraging many of the new technologies mentioned above, we deliver organized, easy to read reports that highlight exactly what you need to know from the search results. Instead of sifting through stacks of filings, you’ll receive clear summaries and copies of all relevant documents, saving you time and effort. Our automated systems and trained experts double-check debtor name variations and filing jurisdictions to minimize the risk of anything slipping through the cracks. And if you’re managing transactions through modern title or closing software, we offer integration options to seamlessly order and retrieve searches without disrupting your workflow.

Ultimately, our goal is to help title agents, lenders, attorneys, and brokers navigate the UCC search process with confidence and efficiency. From a simple UCC lien check on a borrower to a multistate, multifaceted due diligence project, Skyline Title Support can tailor our services to your needs. We stay on top of the latest legal changes (like Article 12 amendments) and continuously update our practices to ensure compliance and accuracy. When you’re ready for a truly thorough lien search and support in clearing any issues that arise, Skyline Title Support is here to assist – providing you peace of mind that your transaction is backed by solid due diligence every step of the way.

Conclusion

UCC searches might not be the flashiest part of a real estate or commercial transaction, but they are undoubtedly one of the most important for safeguarding interests. By mastering UCC search basics, incorporating complementary searches, following a step-by-step workflow, and learning from common pitfalls, you can significantly reduce risk in any deal. And with the advent of new laws and technology, the process is becoming even more reliable and user-friendly. Armed with the knowledge from this guide, you’ll be well equipped to conduct UCC due diligence that is thorough, up-to-date, and effective – giving lenders, buyers, and all parties the confidence to move forward securely. Happy searching, and remember that expert help is available whenever you need that extra assurance in your due diligence process!

Related Posts

If you have ever opened a title commitment and felt your stomach drop when you hit the exceptions, you are not alone. Buyers often see a long ....

January 31, 2026

The title industry is heading into 2026 with more moving parts than at any time in recent memory: rapid regulatory change, deeper fraud risk ...

December 22, 2025

In 1692, the town of Salem, Massachusetts descended into chaos. Fueled by fear, rumors, and suspicion, dozens of people were accused of witchcraft and ...

December 22, 2025

Imagine this: A $3.2 million Miami Beach home sale implodes because of a $127 unpaid utility lien that no one caught in time. Absurd as it sounds ...

December 22, 2025

Recent Posts